If you’ve got crypto sitting idle in your wallet, you’re probably leaving money on the table. This isn’t speculation—it’s fact. You're missing out on potential compounding returns, and that’s how people build real wealth. Not through a 9-to-5. Not through saving pennies. Through smart use of capital.

The good news? There are concrete ways to earn passive income using crypto. The even better news? I’m going to walk you through them—directly, clearly, and without the hype.

Compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t, pays it.

So let’s get started.

What Is Passive Income in Crypto?

In crypto, passive income usually means earning yield. That’s your return, expressed annually as a percentage—APY. But not all yields are created equal.

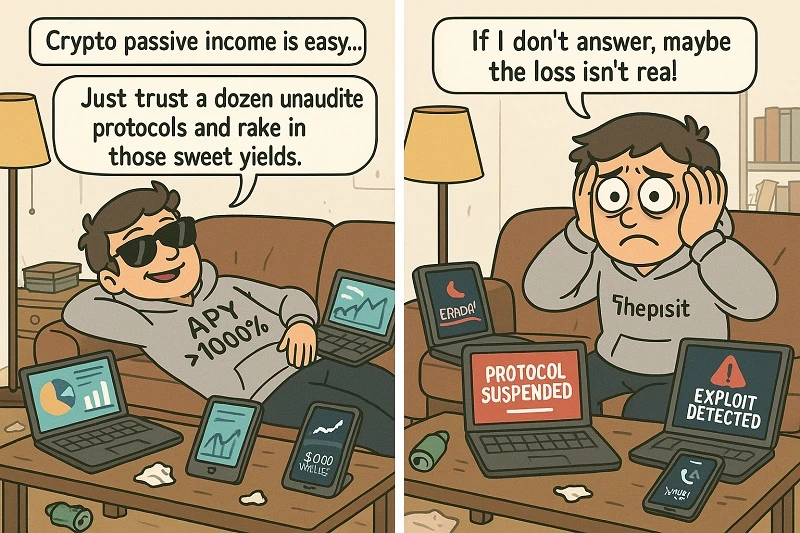

You might see yields of 12,000% somewhere on DeFiLlama or a similar aggregator. Ignore them. They’re bait. Most of the time, high yields like that are paid out via token inflation. In other words, the protocol prints new tokens out of thin air to reward you. It’s not real income—it's dilution.

What you’re after is real yield—returns that exceed inflation, usually coming from actual value creation like fees or borrowing interest. Always ask: What’s the real yield?

Take ATOM, for example. Staking rewards show an average APY of 17.91%. But scroll down and you’ll see the inflation rate: 12%. Your actual return? Just under 6%. Not terrible, but also not what was advertised. And if ATOM’s price is falling (which it has been), even that real yield might not be worth it.

Bottom line: only chase yield on strong assets with long-term viability.

Staking

Let’s start with the most obvious option—staking. If you hold proof-of-stake assets like ETH, you can earn yield by locking them up to help secure the network.

You’ll need 32 ETH to become a validator yourself. If you don’t have that, you’ll stake through someone else—a centralized exchange, a wallet provider, or a dedicated staking protocol.

Staking through exchanges? Not recommended. It centralizes the network and creates a massive attack surface. Even Ethereum’s own foundation warns against it.

Better? Use liquid staking.

Liquid Staking

Liquid staking lets you stake your crypto and still use it. You get a liquid token—think of it as a receipt—that’s pegged 1:1 to your original asset. You can trade it, lend it, or use it in DeFi.

The most common example: stETH, the token you get when you stake ETH via Lido. Lido has a massive market share, staking around 28% of all ETH. While Lido doesn’t run nodes itself—it delegates to 30 independent validators—the risk is still centralized: smart contracts.

If there’s a vulnerability in Lido’s smart contract, the whole system could unravel. That’s not theory—last year, over $2 billion was lost to DeFi hacks, and nearly half of that came from smart contract exploits.

Every interaction with a smart contract is a risk exposure. The more complex your yield strategy, the more code you’re trusting.

Restaking

Restaking (yes, this is a real thing) means redeploying your staked or liquid-staked assets into new protocols to earn extra yield. Think of it as staking your stake. Protocols like EigenLayer allow this kind of stacking strategy.

Sounds smart? Maybe. But again, more contracts, more risk. Restaking isn’t a free lunch—it’s a risk sandwich.

Liquidity Providing (LPing)

Now we dive into decentralized exchanges. DEXs need liquidity to operate, and that liquidity comes from users like you. You supply two assets (in a specific ratio) into a pool, and when people trade, you earn a cut of the fees.

If the pool gets volume, the returns can be solid—especially if you compound earnings. But here’s the catch: impermanent loss.

Impermanent loss happens when the two assets in the pool diverge in price. Your actual return might be negative, even with a good APY.

To minimize this, use assets that are closely correlated—like two stablecoins or ETH and stETH. And always run your plan through an impermanent loss calculator before you commit.

Another tip: LPing manually is not for beginners. Use aggregators that streamline the process. Google is your friend here.

DeFi Lending

If you don’t want the volatility of LPing or the inflation risk of staking, consider DeFi lending.

Platforms like Aave let you lend stablecoins like USDC and earn modest returns (3–5%). It’s not much, but it’s stable and often better than your bank.

Want a bit more yield? Look into Real World Asset (RWA) protocols like Ondo. They tokenize U.S. government bonds. You can earn over 5% on stablecoins like USDY—backed by the U.S. Treasury. Safe? Arguably the safest thing in crypto, because it’s not really crypto—it’s traditional finance ported onto the blockchain.

Centralized Exchange Products

Let’s say DeFi isn’t your thing. That’s fine. Centralized exchanges (CEXs) now offer a suite of passive income tools with cleaner UX.

On Bybit, for example, you’ll find:

- Savings (lending your crypto to other traders),

- Dual Asset products (really just options trading),

- Liquidity Mining (same as LPing, rebranded).

Be aware: These products carry their own risks. For lending, you’re counting on the platform’s liquidation engine to work. For dual asset, you're entering options trading territory—high risk, very much not passive. For liquidity mining, yes, there are nice interfaces and eye-catching APRs, but leverage is often involved. And with leverage comes liquidation.

Always understand what you're signing up for.

Final Thoughts: Be Realistic

Every passive income strategy in crypto comes with trade-offs. Smart contract risk. Platform risk. Inflation. Volatility. Don't get blinded by the shiny APY.

Before diving into anything, Google the compound annual growth rate (CAGR) of Bitcoin. Then ask yourself honestly: Does this strategy have a better risk/reward profile than just buying and holding BTC?

This isn’t a trick question. You don’t need to do anything fancy to win long-term. But if you're going to venture into yield strategies, at least know the landscape. You’re not playing a game—you’re managing risk.

Choose wisely.

Other articles for you

If you're serious about learning how to invest, start by understanding the basics—like dividend stocks

How to build a high-quality dividend stock portfolio from scratch

What if I told you there's a way to transform a simple $10,000 investment into a machine that could pay you thousands of dollars in monthly income during retirement?

Understanding Municipal Bonds: A Direct Guide for Smart Investors

Municipal bonds are far from flashy—but that’s their strength

Learn how to invest in REITs effectively, avoid common mistakes, and build a diversified real estate portfolio with long-term passive income potential.

Let’s clear the confusion

What income will put you in the upper middle class? The answer might be a little more complex than it seems.

No one wants to be broke

Your twenties matter more than you think